Introduce a purchasing card (P-card)

An extract from 50+ Ways To Improve Accounts Payable – Toolkit (70 page Whitepaper + e-templates)

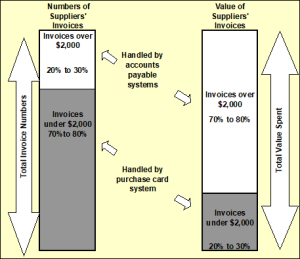

The large study, already mentioned, states that the average cost of the whole purchase cycle has been estimated at $90 per transaction. This is pretty horrific when you realize that a high portion of your transactions are for minor amounts. Exhibit 1 shows a typical profile of AP invoices.

Exhibit 1 The AP invoices that a purchase card is targeting

The bulk of invoices can be for low value amounts, especially if consolidation invoices have not yet been organised. Remember, it costs the same to process a $10 transaction as it does a $100,000 transaction. In addition, is it appropriate to request Budget holders to raise an order in your purchase order system for a $20 transaction? Surely the system is designed around 100% compliance on material invoices, say over $2,000, $3,000, 5,000 depending on your size. Purchase cards, see Exhibit 2 for an example of one, are different from a credit card and are here to stay. In a recent survey conducted by bettermanagement.com 45% said they were using them to some degree.

Exhibit 2 Purchasing Card

There are many controls over purchase card expenditure. To date I have never come across a purchase card fraud and I have spoken to over 5,000 accountants! A card holder has a limit on any transaction, a limit for a daily/ weekly/monthly expenditure, cannot purchase items that do not relate to their function. Different card holders have different settings coded in the magnetic strip. One budget holder may not be expected to entertain or have motoring expenses. Thus, if the card was used at a restaurant or a gasoline station it would be rejected.

Most organisations are happy with this level of control and will accept the sole liability for the card expenditure. However, the ever-cautious organisation can have the liability rest with the staff person and they then need to be reimbursed before the payment is due. This involves the organisation in more processing so it is not the preferred option.

Purchase cards work particularly well when you have organised with the suppliers to also enter the appropriate G/L code information on the transaction. The Two IT functions just need to get together and map out the G/L codes for the supplies and the card informs the supplier of the department code. This is not difficult as most suppliers will not affect more than three G/L codes!

The purchase card is certainly a way for you to take control of processing these minor value / high volume transactions, where they cannot be organised through an electronic consolidated invoice. For more information search the web for “purchase card” + “name of your bank”

“My financial controller lobbied hard for a purchase card for all staff with all expenditure under $2,000 being processed via the card. The staff entered coding for purchases that were not already recoded by the supplier, and the approval process was on-line. Thousands of transactions were replaced by one electronic feed and one direct debit” Quote from a CFO with blue chip international experience

On cut-off day all card holders are given 24 hours or so to ensure all their expenditure is coded. All the purchase card holder has to do is access via the web, the bank’s purchase card system (which off course can be done from an airport lounge), enter their security details to get access to their statement. If they have purchased from a designated supplier all will be coded, thus underpinning national contracts. It will only be the one–off purchases that need coding. The card system is preloaded with around twenty codes most frequently used purchase card G/L codes such as:

- Books & Journals

- Travel

- Subscriptions

- Consumables

- Kitchen supplies

- Advertising

- Training

- Printing

- Catering

- Stationery (where no stationery contract)

- Advertising

- Maintenance & repairs

- Minor computer soft/hardware

- Miscellaneous

AP staff look at the status of statements, send warning emails off, “please code your expenditure by 5 p.m. tomorrow” and where necessary code all un-coded expenditure to an account named “P-card expenditure not coded”.

‘Shame and name’ lists and the odd phone call from the CEO “what do you not understand about the importance of this system?” will ensure lapse behaviour is seen as career limiting!

AP can simply upload all the expenditure straight into the G/L and all the purchase cards are paid by one, yes one direct debit payment!! Now can you understand why most organisations in America use this system!!

The better practices with purchase cards include:

- A minimum amount is set before Accounts payable will process an invoice I would suggest a minimum of $2,000. You need to look at the profile of your expenditure. You want at least 50% of the volume to be caught by the purchase card system.

- All employees who make regular purchases are given a purchase card

- Employees who make only one-off payments do so through their own credit card and claim back or use their manager’s purchase card

- Corporate credit cards are recalled as they represent a duplication

- You never take them away from staff who are not coding their expenditure, you simply set the hounds on them!

- Pick the card holder that offers the easiest system, that links well with you G/L, permits supplier to code, and has a cash expense claim add-on

- For suppliers who are reluctant to lose the 2-3%, offer to reimburse based on the annual spend once a year.

- Supported by a good intranet based procedures manual

These systems have been working well in many companies. All you need to do is contact your bank, they will have many better practice examples. See Appendices 4 and 5 for purchase card guidelines and rules.

The benefits of a P-card are many and include:

- Savings on transaction costs. $90 per transaction via a traditional, paper-based purchase order process to $20 for a transaction via P-card*

- Process simplification. 3 approvals for a $2,000 payment for traditional PO system, to 1.4 approvals for a p-card transaction*

- Increased working capital. A typical p-card transaction provides 29 days of float

- Cycle time savings. Procurement cycle is 9.9 days via the traditional purchase order-based process but only 2.9 days via P-card*.

- Other benefits. P-cards also lead to reductions in petty cash accounts and cash advances, and the avoidance of late fees or lost discounts

* 2017 study of 3400 respondents covering 20 major US and Canadian banks

In the above-mentioned study 80 percent of all P-card spend was conducted by just 20 percent of P-card users. This means that many P-card rollouts had not meet their full potential. To increase use the study recommends emphasizing the importance of:

- supplier engagement

- employee p-card training

- clear P-card spend policies

- the development of performance indicators to measure P-card use

For more information search the web for “purchase card” + “name of your bank”.

Visit the following sites for free access to a good purchase card manual.

- ndsu.edu/purchasing/procurement_card/applyforapcard/

- state.wi.us/vendornet/purchcrd/manual6.pdf

To access more about accounts payable improvements access the 50+ Ways To Improve Accounts Payable – Toolkit (70 page Whitepaper + e-templates)